The Equation of Exchange says:

where:

= Money supply

= Money supply = Velocity of money

= Velocity of money = Price level

= Price level = Real GNP

= Real GNP

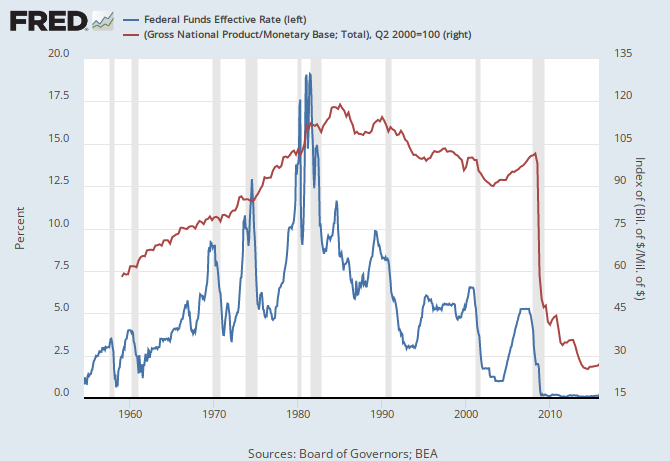

When you first introduce the punchbowl, as the Fed buys bonds or lends to banks cheaply the money supply goes up and the interest rates go down which makes the velocity of money also go down (as seen in the graph above). The lower velocity of money can largely compensate for the increased quantity of money so that the price level does not change too much. It seems like free money has no downside and the central bank has amazing powers.

- However, if you try to withdraw the punchbowl the interest rates also go up, increasing the velocity of money. This increased velocity of money compensates for the reduced money supply so you have the pain of higher interest rates but still get the inflation. It can seem like "inflation is out of control" and the central bank is powerless. This makes for a difficult time for a central bank. It can take a very strong leader and a recession to really get inflation under control.

However, the velocity of money can also go up because of inflation. So if they don't take the punchbowl away you can get inflation because of the increasing money supply and also from the increasing velocity of money. In bad cases this can develop a positive feedback loop and really get out of control.

- John Hussman has a graph showing how extreme the current conditions of low interest rates, high money supply, and low velocity of money are:

- Even a tiny move from 0.125% to 0.25% in the fed funds rate would imply a similar move in 3-month treasuries, which the above graph indicates will cause a large increase in the velocity of money. By the equation of exchange, a large increase in the velocity of money will increase the price level and inflation.

- Update: Jason Smith made a post responding to this one. There are interesting comments here and also on that post.

- Update 12/23/15: two more graphs:

- Graph with fed funds and velocity of monetary base:

- Graph with fed funds and velocity of monetary base less excess reserves. Better fit if we take out excess reserves. Lower interest rates lower velocity and higher raise velocity. Some lag though. I like this view of short term stuff better than Hussman's.

- Since I think excess reserves are really like government debt, and base money should be stuff that does not pay interest and so has a hot-potato effect, I think it is correct to subtract excess reserves from the base money when calculating velocity of money to compare to fed funds rate.

- Update 12/29/15:

- Tom Brown points out that all reserves earn interest and so are not really like interest free money. So I made another graph with all reserves subtracted:

Introducing the punchbowl is easy and removing it is difficult but keeping the punchbowl forever can be deadly.

Vincent, you write:

ReplyDelete"When you first introduce the punchbowl, as the Fed buys bonds or lends to banks cheaply the money supply goes up and the interest rates go down which makes the velocity of money also go down (as seen in the graph above)"

Does "introduce the punchbowl" mean the Fed is holding down rates? John Cochrane disagrees. He thinks the banks are actually loaning the Fed those reserves:

"Well, let's think about that. If a central bank were holding down rates, what would it do? Answer, it would lend a lot of money at low rates. Money would be flowing out the discount window (that's where the Fed lends to banks), to banks, and through banks to the rest of the economy, flooding the place with low-rate loans. The interest rate the Fed pays on reserves and banks pay to borrow from the Fed would be low compared to market rates; credit and term spreads would be large, as the Fed would be trying to drag down those market rates."

"That is, of course, the exact opposite of what's happening now. Banks are lending the Fed about $3 trillion worth of reserves, reserves the banks could go out and lend elsewhere if the market were producing great opportunities. Spreads of other rates over the rates banks lend to or borrow from the Fed are very low, not very high. Deposits are flooding in to banks, not loans out of banks."

And he's not the only one. I read the same thing from an economist in a very different school of thought recently (I think it was Brad DeLong... I'll try to dig it up).

It wasn't Brad DeLong, it was Krugman!... Ha... Cochrane and Krugman are usually at each others throats, but on this point the liberal Keynesian and the conservative supply sider neo-Fisherite agree: the Fed isn't loaning the banks reserves, the banks are loaning the Fed reserves:

Delete"Incidentally, this also means that the common claim that QE is a giveaway to bankers is the opposite of the truth; to the extent that journalists with close ties to bankers spread this story, it’s Orwellian. Remember, the Fed isn’t lending money at low interest to banks — banks, with their $2.5 trillion (!) of excess reserves, are lending vast sums at low interest to the Fed."

BTW, that Krugman post I linked to here is one in a series he's been doing on "Permahawkery" and why he thinks it exists.

I pointed out to John that he agrees with Krugman there. We'll see if he allows that comment through. Lol.

DeleteBut beyond that, Jason Smith, the Market Monetarists, Cochrane (a neo-Fisherite) and Keynesians (like Krugman, DeLong and Simon Wren-Lewis) are all on the same page on this... Why raise rates when inflation and inflation expectations (and NGDP levels and NGDP level expectations) are so low? Nunes and his minions (James Alexander and Ben Cole) have in fact been arguing vehemently that rather than raising rates, the Fed should finally be getting rid of IOER.

In fairness, I think Smith is the least worried about leaving rates low from that bunch. In fact, I have the impression he doesn't actually think it matters too much (I could be wrong about that impression though). However I know he did write that he would not raise them now.

In a more recent post, Jason Smith argues that many different schools of thought (monetarist, Keyneisans, neo-Fisherite, etc) can trace their linage back to Knut Wicksell and his concept of the "natural rate." Jason speculates that this might actually be something that doesn't exist.

DeleteScott Sumner actually seems to be echoing some of Krugman's series on what's behind this push by finance industry executives to raise rates:

Delete"The Fed can’t magically produce strong long run real returns on investment for insurance companies, especially with tight money. That’s far beyond their powers, according to all models I’m aware of (monetarist, Keynesian, Austrian, etc.) If Bill Gross has a new model, I’d love to see it. In the 21st century, insurance companies will have to learn to live with lower returns. They may have to raise the price of insurance. If they lose business, then . . . well, tough luck!"

That's from Sumner's criticism of Bill Gross's call to raise rates.

More from Scott today.

DeleteI think Scott would argue that the punch bowl was taken away a long time ago and that we are suffering the effects of tight money right now. I think his basic calculus is this:

NGDP expectations low = tight money

NGDP expectations high = loose money

Interest rates, etc, don't really come into play. Other than (as Milton Friedman pointed out) as an indication. For example, when rates are low it's a typical sign that money has been too tight. When rates are high, it's a typical sign that money has been too loose.

I'm not saying I agree with Scott, or even that my oversimplification is adequate to represent his views, but nonetheless, it's one of the many mutually incompatible ideas out there that has a certain following: an indication that macro science has a LONG time (centuries?) to go to settle some of this.

Tom, about what Krugman wrote "banks, with their $2.5 trillion (!) of excess reserves, are lending vast sums at low interest to the Fed." Here's my thinking, the interest rate on reserves has to be compared in terms of risk, liquidity and yield to other options. One month treasury yields are at 0%. Compared to that the banks are making a great deal.

DeleteAs far as the economy and banks are concerned, loaning money to the government and loaning money to the Fed has the same effect. It gets some money out of circulation, reducing inflation pressure, and the bank earns a bit of interest. The risk of huge government debt is the same as the risk of huge money at the Fed, that suddenly people want their money back and start spending it, causing inflation.

Deletehttp://howfiatdies.blogspot.com/2013/02/excess-reserves-is-like-government-debt.html

Right so Krugman claiming that the banks do Fed a favor by lending at 0.25% doesn't make sense when the market price available to others for lending to the Government at similar duration is at 0%.

DeleteMy point is that when looking at the risk of hyperinflation you should take government debut plus bank excess reserves divided by GNP. That as far as the danger of runaway inflation, excess reserves are just like government debt.

DeleteVincent, on another topic, have you followed the debate instigated by Paul Romer about scientific integrity in macro? He's drawn lots of critics from all sides of the argument, complaining that he's gone too far, that he's mischaracterized other economists, and complaining that he hasn't gone far enough as well. But putting aside most of the specifics of his historical analysis and his analysis of his current fellow macro economists, I think his invocation of what he dubbed "Feynman integrity" as a standard all should strive for was interesting, and I agree with him on that. Here's the article in case you missed it (like I say, it's one in a series of posts on this topic on his blog):

ReplyDeletehttp://paulromer.net/feynman-integrity/

Here's the bit about Feynman integrity:

----------------------------------

But then, if I have any integrity at all, I have to hold myself to the standard I’m proposing for others. In another twitter exchange, someone linked to a commencement address by Richard Feynman that described what this type of integrity entails:

"It’s a kind of scientific integrity, a principle of scientific thought that corresponds to a kind of utter honesty–a kind of leaning over backwards. For example, if you’re doing an experiment, you should report everything that you think might make it invalid–not only what you think is right about it: other causes that could possibly explain your results; and things you thought of that you’ve eliminated by some other experiment, and how they worked–to make sure the other fellow can tell they have been eliminated.

Details that could throw doubt on your interpretation must be given, if you know them. You must do the best you can–if you know anything at all wrong, or possibly wrong–to explain it. If you make a theory, for example, and advertise it, or put it out, then you must also put down all the facts that disagree with it, as well as those that agree with it. There is also a more subtle problem. When you have put a lot of ideas together to make an elaborate theory, you want to make sure, when explaining what it fits, that those things it fits are not just the things that gave you the idea for the theory; but that the finished theory makes something else come out right, in addition."

Call this Feynman integrity. It forces me to say that a blog post that I write is not a news article that has been fact checked and vetted by an editor. It is me, putting my reputation on the line, saying what believe is true. Nothing more. Treat it with the appropriate degree of skepticism.

--------------------------------------------

I'm curious what your thoughts are about this. IMO the state of affairs in macro today is reminiscent of medical science in the Medieval Europe: there are blood letters, cuppers, ear candlers, etc, all with high levels of confidence in their various methods, but any outside observer should be able to tell immediately that most of that is incorrect since they don't agree with one another. Modern medical scientists at least agree about the basics. Sure there's plenty to disagree about on the fringe, but then you don't often here a lot of confidence being expressed there. Similar to how physicists all agree about basic quantum theory and thermodynamics, but perhaps disagree about string theory or the multiverse theory. But you don't hear any physicists expressing certainty in a fringe theory (unless they're a crank)! Unfortunately in macro, it appears to be almost ALL fringe (with very little core) based on the level of substantial disagreement that exists. What seems odd to me though is why so many macro economists express high confidence in their non-consensus ideas. Sure, perhaps one of them is correct... *maybe*... but it necessitates that the rest are wrong. The other possibility, of course, is that all of them are wrong.

I think it's fair to say that most of the prominent macro economists who publicly blog or otherwise make public statements concerning macro are wrong, but more concerning to me is that they're also terrible at estimating an appropriate level of confidence to have in their speculative hypotheses. Logically, most all of them necessarily must be wildly over estimating (or at least publicly over stating) their level of confidence. It's almost like they're not really scientists at all, and instead are merely rhetoricians.

DeleteHey Tom! Before I get into your 8 comments, what did you think of the main idea of this post that velocity of money depends on interest rates and inflation rates and if the Fed starts to raise at all the velocity of money starts to go up?

ReplyDeleteYour graph seems to indicate that there's a correlation between the velocity of MZM (that's a pretty broad definition of money isn't it?) and 10 year interest rates, yes.

DeleteWhether or not it's a casual relation is another story I suppose. Mark S. might think you should do a procedure like this to find out:

http://davegiles.blogspot.com/2011/04/testing-for-granger-causality.html

I'm not sure Jason would agree in this case.

You almost sound like a neo-Fisherite with that view. Why don't you run it past Stephen Williamson?

I saw your post at Cochrane's, and your lead sentence contradicts his post. We'll see how he responds! He doesn't respond that frequently unfortunately, ... well, at least not to me.

The more I learn, the less certain I am of any of this stuff.

Thanks. I posted a comment asking Stephen Williamson for feedback.

DeleteThanks much. I am still sure I am right on hyperinflation being a positive feedback loop. Less sure of other things. :-)

Saying that velocity has anything to do with the pricing of money other than a marginal effect of changing the liquidity contradicts the backing theory. I believe money is backed by the financial power of the government and as such velocity does not matter much to its pricing.

DeleteInteresting argument Dan. I think you would be on strong ground if the backing was real bills or gold but when the backing is debt in the same currency the value of the debt drops with a rise in the interest rate. More important the backing theory does not really provide a value of the currency relative to anything else if the backing is debt in the same currency.

DeleteVincent, the way I see it, according to the backing theory the market will provide a value of the currency relative to everything else and this will happen regardless of if the backing is debt in the same currency. If an enormous earthquake hit Japan wiping out a big part of their productive capacity while their debt obligations stayed the same the currency would crash right away. The market know things have changed fundamentally and the currency would be reevaluated. Velocity or printing would happen as a response, not as a cause.

DeleteIn the backing theory the value of the currency is the number of bills divided by the value of the assets. But if the assets are bonds in the same currency it is like the value of the currency is defined in terms of the future value of the currency. It is not well defined. If you look at a country with hyperinflation in terms of the backing theory the value of the long term bond assets are crashing as the currency is crashing and the interest rates and inflation rates are going up. But as the inflation and interest rates go up, the bonds crash more, so the backing for the currency is lower. This can be a positive feedback loop. The core idea of the "Real Bills Doctrine" was that you must not be holding long term bonds in your own currency, but things of real value outside the currency or very short term debt like 30 days. This was the only way to play it safe. Central banks today have forgotten this wisdom and I think there will be lots of chaos because of this.

Deletehttp://www.csun.edu/~hceco008/realbills.htm

If we are just debating the validity of the theory then even if it would be hard for the market to figure out a value it doesn't mean that the market can't do it. The way I see either the backing theory or the equation of exchange (other than as a tautology) must be false. Velocity can not both be a factor in inflation and not be a factor.

DeleteThe market will figure out a value, but it can change really fast if all the assets are bonds denominated in the same currency. It is unstable. The Real Bills warns you not do have long term debt in the same currency banking your currency as that is dangerous and you may see your currency crash. Not that the market won't have a value. I don't see any contradiction between the two and see both as correct.

DeleteThe very name "Real Bills" is saying if you have real assets then your can issues as many notes as you have assets and the notes will not lose value but it means compared to these real assets. So the velocity of the currency would not matter. You could say the velocity of the assets changed their value though. Real Bills is like a currency peg. The East Caribbean Dollar has been pegged at 2.7 to the US dollar since 1976. They are really using US dollars like Real Bills plan would have used gold. The velocity of the EC dollar does not risk the peg in any way, as they always have enough assets to hold the peg.

DeleteThe velocity of the currency never matters (much). That's what the backing theory claims. Just as velocity doesn't matter for other financial assets such as stocks. While in Equation of exchange used as a predictor of inflation velocity is one of the determining factors. Both can't be right.

DeleteThe backing theory does not work if the backing is bonds denominated in in the same currency. We seem to be going in circles.

DeleteWell I don't understand what you mean with "does not work" if you agree that the market will figure out a value even if the backing is bonds of the same currency. That value, that the market will figure out, whatever it is will determine the price of money and will have nothing to do with the velocity of money. So you can't be saying both that the market will figure out a value independent of velocity (backing theory) and that the value will be a function of inputs where velocity is one of them (Equation of exchange).

DeleteBy "does not work" I mean if your bank's assets are not real things, then you are not doing "Real Bills" and your notes are not tied to anything in the real world. If your assets are long term bonds their value can crash as interest rates go up and the value of the currency goes down. If the banks asset value is crashing, their currency is crashing by the backing theory. So it is not stable.

DeleteHere is more on Real Bills and hyperinflation: http://howfiatdies.blogspot.com/2013/09/the-real-bills-doctrine.html

DeleteBy does not work, I mean with backing theory and long term bonds as assets you can still get hyperinflation.

In physics there are times where you can solve a problem using "conservation of energy" or using "conservation of momentum". Both ways will give you the correct answer if done right. I think backing theory and velocity of money are like this. Both can work if done right. There is no contradiction.

DeleteOk but "real bills" as a policy of preventing hyperinflation is something different than the backing theory as a theory of explaining inflation. In the "backing theory" the type of backing doesn't matter as far as the functioning of the theory is concerned.

DeleteTo prevent inflation the backing has to be tied to real things. If it only has bonds denominated in the same currency then the inflation relative to real things can be anything. The theory still functions but without proper backing there can be inflation. It still explains it. As you see the bond values in the backing crash because interest rates go up, the currency crashes too. So the theory does function in that sense.

DeleteTo make this concrete lets look at Japan. The backing the Bank of Japan holds is mostly JGBs which are denominated in Yen. If interest rates ever go up the value of these bonds can crash. If they crash, then by the backing theory, we expect the Yen to crash.

DeleteI agree with your example of Japan but my point is only regarding the velocity component of inflation. The point is that the backing theory eliminates velocity as a major part of why inflation happens while in EoE it's the opposite. Even if the BOJ backed its currency with gold there would be inflation if they for some reason lost half of it, according to the Backing theory. That inflation would then have nothing to do with the velocity of the currency. So we have one theory that claims that velocity doesn't affect the value of money and one that claims the opposite.

DeleteIn 1857 the SS Central America was carrying 30,000 lbs of gold for banks in the US and sunk in a hurricane. This lead to the Panic of 1857. If we look at this from a backing theory we see the banks lost some of their backing and their notes become worth less. If we look at it from a EoE view we see the velocity of money going up and notes worth less. You really can look at it either way and understand what is going on.

Deletehttps://en.wikipedia.org/wiki/SS_Central_America

https://en.wikipedia.org/wiki/Panic_of_1857

Here is another way to look at it. If you really had gold backing then by the backing theory the prices of the notes would be stable relative to gold. If prices are stable, then by the EoE you will have stable velocity of money. Both will be correct.

DeleteThe EoE normally is assuming one currency is for the whole country. Back in 1857 there were different banks issuing notes, so I think you have to look at all of them and gold together, but since people also stopped using paper money and switched to real gold the portion of the economy using paper for the EoE got smaller. It is a bit messy as an example really.

DeleteBut here is my challenge to you. Do you think you can find a country with a single currency where the backing theory and EoE can not both fit the data for some period?

This book was mentioned by Mike Sproul: Thomas Sargent, "The Ends of Four Big Inflations". It has data on the weimar inflation and other in it.

Deletehttp://faculty.ses.wsu.edu/rayb/420/Sargent_end%20of%204%20inflations.pdf

"Table G4 documents a pattern that we have seen in the three other

hyperinflations: the substantial growth of central bank note and demand deposit liabilities in the months after the currency was stabilized. As in the other cases that we have studied, the best explanation for this is that at the margin the postinflation increase in notes was no longer backed by government debt."

Page 84

They say "not backed at the margin" but really the central bank keeps printing money and buying government bonds. So there is backing, even at the margin. However, the backing is bonds in the same currency. Those bonds are dropping in value as inflation rates and interest rates go up and because the currency is dropping. By the backing theory, if the backing is dropping, the currency is dropping. But as the currency drops the bonds drop. So you get a positive feedback loop and the currency keeps dropping. This is why the "real bills" says you can not use bonds in your own currency for backing. Wisdom long forgotten. The world will pay for forgetting this.

DeleteI think that at the margin there was a more "real" backing and that was the explanation for the stabilization. That would be something that is hard to fit in to the EoE considering there was still money growth. One might argue in EoE terms that stabilization occurred due to a decrease in velocity or increase in economic output, but it seems far fetched. EoE might still hold true as a snapshot (tautology) meaning that when a variables of one side of the equation changes something on the other side also changes but it wouldn't necessarily explain what causes inflation and it wouldn't necessarily mean that changes in one single variable of the equation would lead to a change in one single other variable. For instance a change in velocity does not have to lead to a change in the price level. One might look at EoE thinking all else equal a change in V will lead to a change in P but V is never measured but a result of the other three variables so it might very well be that a change in V never leads to a change in P in the real world while EoE still holds true but is more or less useless for predictions. Friedmans solution to this problem was to claim that V was more or less stable in the economy which we now know it isn't.

DeleteI don't agree that EoE is useless for making predictions. I use it in my simulation of hyperinflation and think with enough data and work that it could actually get reasonable at making predictions. http://howfiatdies.blogspot.com/2013/03/simulating-hyperinflation.html

DeleteI too think Macro is in a very poor state. I think a big part of the problem is that some groups look at the short term, like if we print more money our GNP number will go up this quarter, and some groups look at the long term, like when you start printing lots of money it is very hard to stop and the end result is very painful for the economy when the bubble pops or the inflation picks up. If they made it clear they were talking about 3 month horizon or 5 year horizon, or whatever, many of the times it seemed like they were disagreeing with each other would go away.

ReplyDeleteI do think that some sort of Feynman like honesty ethics would be a good thing for Macro.

The "punchbowl" means "easy money" which means the Fed is making money and loaning it to banks or buying bonds. At first this makes interest rates lower than if they were not doing that but if the market get scared of what they are doing, it could be the more they print the higher interest rates go and if they could then stop interest rates would go down.

I like Hussman's explanation of the impact of low interest rates on investments. It is not really changing the earnings of the company or the long term value of the companies income stream, it is just moving the stock appreciation forward. Any increase we get now in the stock we will not get later, so it is not really a net win.

The natural rate is the interest rate we would have if the Fed was not changing the money supply. Don't see any way to really know what it would be, but I am sure that 0% is not the natural rate.

ReplyDeleteI commented on both Jason and Grumpy's blogs.

ReplyDeletehttp://informationtransfereconomics.blogspot.com/2015/09/the-classical-mechanics-of-wicksell.html?showComment=1443131122291#c20225450472562111

http://johnhcochrane.blogspot.com/2015/09/is-fed-pulling-or-pushing.html

Jason made a post out of his reply to you. I think you'll find it interesting!

DeleteYes, very cool. Tom, you are doing a good job of cross-pollinating economics blogs! Thanks!

DeleteVincent, maybe you can help Tyler Cowen explain this puzzling development.

ReplyDeleteThanks, I commented there too.

DeleteVincent- Since you are predicting hyperinflation as a result of the "punchbowl", can you make a specific prediction of a time frame in which you expect such hyperinflation. I would also like to know if there is a specific time frame in which you might reconsider your hypothesis if the expected hyperinflation does not materialize, thanks.

ReplyDeleteI am confident hyperinflation is a positive feedback loop like an avalanche, forest fire, or earthquake. I think I have good theory on the mechanism for hyperinflation. However, for when/where it will trigger/start I don't really have good theory. It is the difference between understanding what is going on in an avalanche and being able to tell when it is going to start. Here is what I mean:

Deletehttp://howfiatdies.blogspot.com/2014/08/positive-feedback-theory-of.html

That said, I am expecting hyperinflation in Japan with inflation picking up fast sometime in the next couple years but this is more of a guess or hunch and not really an application of solid theory about timing. If Japan gets it then I think others will follow and things will get really bad all over.

Fair enough, let's say 3 years. How long would it take for Japan not to have hyperinflation before you consider a different model for inflation?

DeleteIf either Japan or the USA is able to raise rates back to even 3% on the short-term without causing the velocity of money to shoot up, and hence inflation shooting up, my model on this page would be shown wrong.

DeleteJapan has bought more than 1/4 of all outstanding JGBs so far, if they are able to get past 50% without triggering a positive feedback loop of people dumping the bonds and inflation going up fast, I would consider a different model for hyperinflation.

I want to say something even a bit stronger than "I don't have a good theory to predict the timing". I believe it may not be possible to predict the timing. Something that is just not possible for us to predict the timing on might be the trigger. For example maybe ISIS attacks Saudi Arabia's oil handing ports and suddenly oil is more expensive. Or maybe some ships from China and Japan exchange missiles. It is like having a big pile of gunpower and a spark generator that is just out of reach. At some point one spark is going to go extra far and light off the whole pile but you can't predict ahead of time exactly when.

Delete... but perhaps that pile of gunpowder is a lot more all encompassing, and hyperinflation will be the least of our troubles should it catch fire.

DeleteI can predict a collapse in world wide GDP... should a cubic mile sized asteroid impact the Earth. I don't see any on the horizon, but you never know when something like that is going to show up on the radar.

Tom, I think the theory I have is enough to make money with. I can get 100:1 odds/payoff on Japanese hyperinflation in the next 2 years and my theory can give me confidence that the chances of Yen hyperinflation are much greater than 1 in 100 over the next 2 years, it is seems like I have a good chance of profiting from this insight. I am not sure how knowing that there are asteroids that might hit the Earth can help you make money. So I think my theory/predictions are far more useful than yours.

DeleteVincent, regarding predicting when hyperinflation hits Japan, take a look at this:

ReplyDeletehttp://rationallyspeakingpodcast.org/show/rs145-phil-tetlock-on-superforecasting-the-art-and-science-o.html

I got mentioned as "reader Vince" in Mish's blog. This is one of the most popular economics blogs.

ReplyDeletehttp://globaleconomicanalysis.blogspot.com/2015/11/swiss-bank-hits-customers-with-negative.html

My comment there was:

Reader Vince and John Hussman think that interest rates have a big impact on velocity. I also think that inflation rates have a big impact on velocity. If you can predict changes in velocity from something like interest rate and inflation rate then it is a useful concept to an investor trying to predict the future of other things, like inflation.

http://howfiatdies.blogspot.co...

http://www.hussmanfunds.com/wm...

Nice Vincent. If there are still excess reserves when the Fed raises interest rates, then rather than "unwind" the excess reserves, perhaps they will just raise rates by increasing IOR. Do you think?

DeleteTo me it seems nearly certain that the velocity of money must go up as the interest rate goes up. I don't think it is possible to just increase interest on excess reserves and prevent this. In fact, I would expect reserves to go down even if they raise rates on excess reserves. The higher the rates, the higher the velocity, and to increase velocity probably money that was excess reserves and standing still goes back into circulation. The math sort of has to work out.

DeleteSumner says, "Higher interest rates raise velocity. Period. End of Story":

ReplyDeletehttp://www.themoneyillusion.com/?p=18812

I claim the full story must include "higher inflation rates also raise velocity".

Interesting how there was a "premature" (as Sumner put it) rise in interest rates in 1937, followed by them soon plummeting back to zero. He also says that rates should be considered short term rates minus IOR, which has been negative recently (or recently when Sumner put that post up in 2013).

DeletePerhaps the recent rate rise will mimic 1937. Why wouldn't it? What's different?

In fact, looking at Sumner's plots, one might conclude that it won't be for another 40+ years that high inflation will be a problem again.

"What's different?" ... well, to answer my own question, lots of things!... However, what, in your opinion, is of crucial importance?

DeleteNote for future reference. In a comment on Jason's reply post, John Handley says that velocity being a function of interest rate is implicit in the IS-LM model. Since IS-LM is a current fundamental model of macroeconomics, I find this interesting. It seems to be true but not often explained that way.

ReplyDeleteDid you see Nick Rowe's recent posts (also touching on pieces by David Andolfatto and Miles Kimball) about an upward sloping IS curve?

Deletehttp://worthwhile.typepad.com/worthwhile_canadian_initi/2015/12/upward-sloping-is-curves-after-miles-kimball.html

http://worthwhile.typepad.com/worthwhile_canadian_initi/2015/12/upward-sloping-is-curves-simple-version.html

http://worthwhile.typepad.com/worthwhile_canadian_initi/2015/12/tight-money-as-binding-output-quota.html

No. Thanks.

DeleteMish points out that for other measures of money supply the velocity is not tracking the interest rate. Hussman shows that it does for very short term and I show that for MZM and 10 year it does, but for lots of other things in the middle it does not track. This is interesting. If someone could explain this I would appreciate it. :-)

ReplyDeleteHere's another guy pointing out that curve Vincent:

ReplyDeletehttp://www.philipji.com/item/2014-04-02/the-velocity-of-money-is-a-function-of-interest-rates

I think you've encountered him before if I'm not mistaken.

Very cool. I had not seen that graph. That is a nice fit. His Corrected Money Supply and AAA bonds works too then.

DeleteI am terrible with names but don't remember him. Google does not seem to find any pages with both his name and my name on them.

Note that my March 24, 2013 post and my hyperinflation simulation used the idea of the velocity of money depending on the interest rate. It was really the key to getting the simulation to work. So I did not get it from his 2014 post. :-)

DeleteLinks are free and maybe some reader will want it:

Deletehttp://howfiatdies.blogspot.com/2013/03/simulating-hyperinflation.html

I *think* he used to go by "phil" on pragcap (and other) comments. Cullen and he got into it on a regular basis. If it's the same guy I'm thinking of.

DeleteAnd another couple:

ReplyDeletehttp://informationtransfereconomics.blogspot.com/2016/01/scott-sumner-latest-information.html

That links to this:

Deletehttp://www.themoneyillusion.com/?p=31387

Which shows money demand vs interest rate. So it is showing the same thing, but velocity vs interest rate makes it far easier to see the connection.

This post and comments now makes up some real research on velocity of money and interest rates!

Thanks again!

Yet more on this topic Vincent:

ReplyDeletehttp://informationtransfereconomics.blogspot.com/2016/01/velocity-of-money-and-interest-rates.html

Thanks again Tom!

ReplyDelete